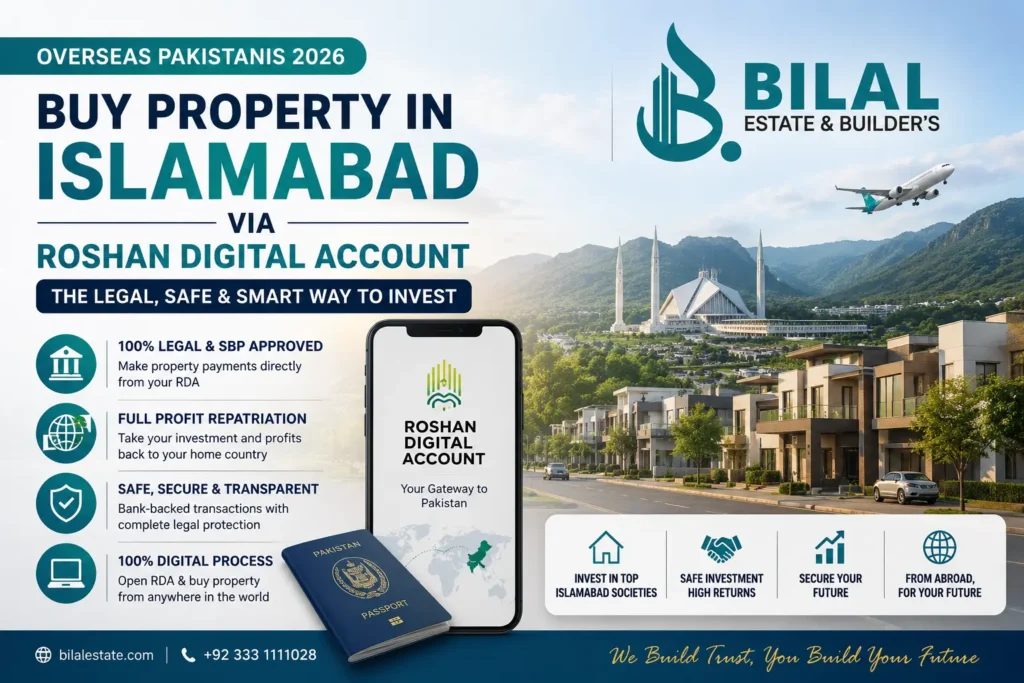

How to Buy Property in Islamabad via Roshan Digital Account as an Overseas Pakistanis 2026

You can buy property in Islamabad via Roshan Digital Account (RDA) by opening an RDA with any SBP-authorized bank, funding it in PKR or foreign currency, and making all property payments — including token money, down payment, and full purchase price — directly from your RDA PKR account. The process is fully digital and legally qualifies you for full profit repatriation.

The Mistake Thousands of Overseas Pakistanis Are Still Making

You’ve been sending money home for years. Your parents manage the transaction. Your cousin “handles” the paperwork. And somewhere between the power of attorney, the grey-market dealer, and the verbal agreements — your money is sitting in someone else’s property, half-legally, with zero protection.

This is not a rare story. It’s the default story for overseas Pakistanis who buy property without using the RDA system.

Here’s the hard truth: if you didn’t buy property through your Roshan Digital Account, you may not be able to legally repatriate the profits when you sell. You might owe taxes you didn’t expect. And if anything goes wrong, you have very limited recourse.

But there’s good news. Pakistan’s Roshan Digital Account system has made it genuinely possible — and surprisingly straightforward — to buy property in Islamabad from anywhere in the world, with full legal protection and the right to take your money back out when you need it.

This guide walks you through every step. Whether you’re in Dubai, London, Toronto, or Riyadh — this is what you actually need to know.

What Is the Roshan Digital Account and Why Does It Matter for Property Buyers?

The Roshan Digital Account (RDA) is a banking initiative launched by the State Bank of Pakistan (SBP) in September 2020, designed specifically for Non-Resident Pakistanis (NRPs). It allows overseas Pakistanis to open and operate a fully functional Pakistani bank account — without ever visiting a branch.

But it’s much more than a bank account.

For property buyers, the RDA is the legal gateway to investing in Pakistani real estate with what’s called repatriable status — meaning the money you invest, along with any profits or rental income, can be sent back to your foreign bank account without restriction.

When it comes to how to buy property in Islamabad via Roshan Digital Account, the process is legally clean, bank-backed, and increasingly popular.

In this guide, you’ll learn:

- How RDA works for property purchases

- The step-by-step buying process

- Which Islamabad societies are best for RDA investors

- Common mistakes and how to avoid them

- All 15+ FAQs answered clearly

Why This Matters: The Key Benefits of Buying Property via RDA

1. Full Repatriation Rights

This is the single biggest advantage. When you sell a property purchased through RDA, you can legally transfer the full sale proceeds — principal plus profit — back to your foreign bank account. No RDA purchase means no guaranteed repatriation.

2. Legal Protection from Day One

All payments go directly to the seller from the bank, through a banker’s cheque. No cash, no middlemen handling your funds. The paper trail is clean.

3. Invest Jointly with Family

You can purchase property in your own name or jointly with immediate family members — spouse, parents, siblings, or children. This is ideal for families planning a future home together.

4. Tax Simplicity

RDA holders benefit from a simplified tax regime introduced by the Federal Government. The profits, rental income, and capital gains from RDA-backed property can be deposited back into your RDA and repatriated.

5. Financing Available (Roshan Apna Ghar)

You don’t need to pay the full amount upfront. Major banks — HBL, Meezan, Bank AL Habib, JS Bank — offer housing finance under the Roshan Apna Ghar scheme, specifically for RDA holders. Financing up to PKR 100 million is available with tenures up to 25 years.

6. Complete Digital Process

From account opening to property purchase, the entire process can be done without physically being in Pakistan. Your nominee in Pakistan can execute certain steps on your behalf.

Data and Facts: The Numbers Behind RDA Real Estate Investment

The RDA program has grown at a pace few expected. Here’s where things stand:

- As of February 2026, more than 900,000 Roshan Digital Accounts have been opened, with total inflows exceeding $12 billion — according to Pakistan’s Finance Minister Muhammad Aurangzeb.

- Pakistan recorded historic remittances of over $38.3 billion in FY2025, a 26.6% increase year-on-year. The government expects this to reach $42 billion in FY2026.

- In October 2025 alone, $3.4 billion in remittances were recorded — a 12% jump from the previous year — with much of it going into high-trust property projects like DHA and Bahria Town.

- Islamabad’s residential property market has seen approximately 10.5% annual price appreciation, with experts projecting 3–7% growth in prime urban housing from late 2025 through mid-2026.

- The real estate sector in Pakistan is expected to grow at a 4% CAGR between 2025 and 2029, contributing nearly 2% to Pakistan’s GDP.

These are not speculative numbers. They come from SBP data, Pakistan Today, and market research published in late 2025. The trend is clear: overseas Pakistani investment in domestic real estate is structural, not cyclical.

A Real Example: How Ahmed Bought a House in DHA Islamabad from Toronto

Ahmed, a software engineer living in Toronto for 12 years, wanted to buy a 10-marla house in DHA Phase 2, Islamabad for his aging parents and as a long-term asset.

Here’s what his timeline looked like:

Month 1: Ahmed opened a Roshan Digital Account with Meezan Bank online. Uploaded his NICOP, passport, and proof of residence in Canada. Account was active within 48 hours.

Month 2: He transferred CAD equivalent to PKR 22 million into his RDA PKR account via international wire transfer. He also identified a property through a trusted agent — Bilal Estate and Builders — who handled site visits and legal due diligence on his behalf.

Month 3: Ahmed applied for Roshan Apna Ghar financing through Meezan Bank for a top-up of PKR 8 million, keeping his RDA balance as a lien. The bank’s legal team verified the property title, conducted a valuation, and prepared the sale agreement.

Month 4: The bank issued a banker’s cheque in the seller’s name. Ahmed’s nominee in Pakistan — his brother — was present at the registrar’s office for title transfer. Ahmed signed the legal documents from Canada and couriered them back.

Today: The property is fully in Ahmed’s name. His parents live there. He earns rental income that gets deposited in his RDA — and he knows that when he sells, every rupee of profit comes back to him legally.

The process worked. Not because it was lucky — but because every step went through the proper RDA channel.

Expert Insight: What Actually Works (And What Doesn’t)

After observing hundreds of overseas property transactions, a few patterns are consistent:

What works:

- Choosing possession-ready or near-possession properties in Islamabad’s prime societies (DHA, Bahria Town Phases 1–6, Park View City, Gulberg Greens). These have the least legal ambiguity and the most liquid resale markets.

- Working with a registered, reputable real estate agent who has verifiable RDA transaction experience. Ask specifically: “Have you closed RDA-funded deals before?”

- Making all payments from your RDA PKR account, including token money. Even one payment made outside the RDA breaks the repatriation chain.

- Having a trusted, physically present nominee in Pakistan. Not optional — critical.

What doesn’t work:

- Buying on “files” (pre-possession, unregistered plots) through RDA. The bank requires title verification before disbursing. Underdeveloped or unapproved societies will be rejected at the financing stage.

- Sending money first, asking questions later. Fund your RDA, then begin the property search — not the other way around.

- Using a general power of attorney without a bank-backed process. POAs can be misused; let the bank be the counterparty, not just a family member.

Reality Check: What Nobody Tells You

1. Not all properties qualify for RDA purchase financing. Banks conduct rigorous title verification. Properties in unapproved housing schemes, those with disputed ownership, or those without proper CDA/RDA/LDA approvals will not pass the bank’s legal check. DHA, Bahria Town, Park View City, and CDA sectors are generally safe. Many newer or smaller societies are not.

2. The Roshan Apna Ghar markup rate is not fixed for everyone. Rates are benchmarked to KIBOR (Karachi Interbank Offer Rate). With SBP cutting the policy rate to around 11–12%, financing is more affordable than it was in 2023–24, but it’s still a variable-rate product. Understand your monthly installment before committing.

3. Bahria Town currently carries elevated risk. Due to ongoing legal proceedings involving NAB and Bahria Town’s founder Malik Riaz, market activity has been sluggish and investor confidence is cautious. Prices haven’t collapsed, but transfers have slowed and uncertainty remains. New RDA investors should prioritize DHA Islamabad or CDA-approved sectors over Bahria Town until the legal situation becomes clearer.

4. The process takes 2–4 months minimum. From account opening to title transfer, expect at least 8–16 weeks. Anyone promising faster results is cutting corners.

5. Your nominee cannot make financial decisions for you. Your Pakistan-based nominee handles physical presence requirements (registrar visits, document signing), but all financial instructions must come from you directly through the bank.

Step-by-Step: How to Buy Property in Islamabad via Roshan Digital Account

Step 1: Open Your Roshan Digital Account

Choose an SBP-authorized bank. Major options include Meezan Bank, HBL, Bank AL Habib, JS Bank, UBL, and others. Apply 100% online using:

- NICOP (or POC for lien-based financing)

- Valid passport

- Proof of overseas residence

- Recent photograph

Account activation typically takes 24–48 hours.

Step 2: Fund Your RDA

Transfer funds from your foreign bank account to your RDA. You can maintain both a Foreign Currency Value Account (FCVA) and a PKR Non-Resident Value Account (NRVA). For property purchases, all payments must come from the RDA PKR account.

Step 3: Find and Verify the Property

Engage a reputable real estate agent familiar with RDA transactions. For Islamabad, trusted agencies like Bilal Estate and Builders can assist with site selection, price negotiation, and due diligence. Verify:

- Clear title and ownership history

- Society approval status (CDA/RDA/LDA)

- No existing mortgage or legal disputes

Step 4: Pay Token Money from RDA

Once you’ve decided on a property, pay the token money (advance booking amount) directly from your RDA PKR account. This establishes the repatriation chain from day one.

Step 5: Apply for Financing (Optional)

If you need Roshan Apna Ghar financing, apply through your RDA bank. Submit:

- Application form

- Employer certificate, salary slips (last 3 months)

- NICOP copy

- Property title documents

- Co-applicant documents (if applicable)

Step 6: Bank Legal and Valuation Process

The bank will conduct:

- Property title verification

- Market valuation

- Legal documentation review

This typically takes 3–6 weeks.

Step 7: Disbursement and Title Transfer

The bank issues a banker’s cheque in the seller’s name. Your nominee in Pakistan attends the title transfer at the registrar/society office. You sign legal documents (can be done abroad and couriered). Once the title transfers to your name, the cheque is released to the seller.

Step 8: Maintain Records

Keep all RDA transaction records, bank statements, and title documents. These are essential for future repatriation of sale proceeds or rental income.

Comparison: Best Islamabad Property Options for RDA Investors

| Society | Entry Price (10 Marla) | Risk Level | Repatriation Eligibility | Best For |

|---|---|---|---|---|

| DHA Islamabad | PKR 3.5–6 Crore+ | Low | Yes | Long-term security, stable appreciation |

| Bahria Town (Phases 1–6) | PKR 3.5–6.25 Crore | Medium-High (current legal uncertainty) | Yes | Amenity-rich living, hold with caution |

| Park View City | PKR 1.5–3 Crore | Low-Medium | Yes | Mid-budget, scenic location |

| Gulberg Greens | PKR 1.2–2.5 Crore | Low-Medium | Yes | Growing sector, expressway access |

| CDA Sectors (I-12, I-16) | PKR 0.9–2 Crore | Low | Yes | Affordable entry, long-term appreciation |

For overseas Pakistanis prioritizing legal safety and repatriation certainty, DHA Islamabad and Park View City are currently the strongest options in the mid-to-premium range.

To explore verified listings in these societies, visit Bilal Estate and Builders’ Islamabad portfolio.

Frequently Asked Questions (FAQs)

Q1: Can I buy property in Islamabad via Roshan Digital Account without coming to Pakistan? Yes. The entire process is designed to work remotely. You’ll need a Pakistan-based nominee for physical attendance at the registrar’s office, but all financial transactions and legal document signing can be managed from abroad.

Q2: Which banks offer Roshan Digital Account for property purchase in Pakistan? SBP has authorized multiple banks including Meezan Bank, HBL, Bank AL Habib, UBL, JS Bank, Faysal Bank, and Dubai Islamic Bank Pakistan. Each offers a slightly different product; compare markup rates and processing times before choosing.

Q3: What is Roshan Apna Ghar and how does it work? Roshan Apna Ghar is a housing finance scheme for RDA holders, offered by participating banks. It provides financing up to PKR 100 million for property purchase, construction, or renovation, with tenures up to 25 years. It is Shariah-compliant (based on Diminishing Musharakah) at most banks.

Q4: Can I repatriate the profit when I sell my property? Yes — but only if all payments were made from your RDA PKR account. Rental income and sale proceeds from RDA-funded property can be deposited into your RDA and repatriated to your foreign bank account.

Q5: Can I buy property jointly with my spouse or parents via RDA? Yes. You can purchase jointly with immediate family members: spouse, parents, siblings, or children. At least one co-applicant must be permanently residing in Pakistan if you’re applying for Roshan Apna Ghar financing.

Q6: Is there a minimum or maximum property value for RDA purchase? There is no stated minimum for outright purchases. For Roshan Apna Ghar financing, the minimum is typically PKR 500,000 and the maximum is PKR 100 million for purchase.

Q7: How long does it take to complete a property purchase via RDA? Plan for 8–16 weeks from account opening to title transfer. The bank’s legal and valuation process alone takes 3–6 weeks. Complex transactions or documents sent by courier from abroad may extend this timeline.

Q8: What types of property can I buy through RDA? According to SBP guidelines, you can purchase residential and commercial properties, including plots, houses, apartments, land, and already-constructed properties in new or existing housing schemes.

Q9: Do I need to pay capital gains tax on RDA property? RDA holders benefit from a simplified, favorable tax regime. Profits from RDA investments, including real estate, are subject to capital gains tax under Pakistani law, but the process is streamlined for NRPs. Consult a Pakistani tax advisor for your specific situation.

Q10: Can I rent out the property and send the rental income abroad? Yes. Rental income from RDA-funded property can be deposited into your RDA account and repatriated to your foreign bank account.

Q11: What happens if I want to sell the property later? The sale proceeds are deposited into your RDA account, from which you can repatriate them freely. Keep all original purchase documents, RDA transaction records, and title deeds.

Q12: Is DHA Islamabad a good investment for RDA buyers? DHA Islamabad is widely considered one of the safest real estate investments in Pakistan due to its government backing, consistent price appreciation, legal clarity, and high rental demand. It’s particularly well-suited for long-term RDA investors. See current DHA listings on Bilal Estate and Builders.

Q13: Can resident Pakistanis also use the Roshan Digital Account? Resident Pakistanis can open an RDA, but only in foreign currency. The property purchase and repatriation benefits primarily apply to Non-Resident Pakistanis (NRPs).

Q14: What documents do I need to open a Roshan Digital Account? You need a valid NICOP (or POC for lien-based financing), a valid passport, proof of overseas residence, and recent photographs. The application is completed online through your chosen bank’s website or app.

Q15: What is the risk of investing in unapproved housing societies via RDA? Significant. Banks will not finance or process payments for properties in unapproved societies. Even if you attempt a direct purchase outside bank channels, you lose repatriation rights. Always verify CDA, RDA, or LDA approval status before committing.

Q16: Can I use RDA funds to buy a plot and build a house later? Yes. RDA funds can be used for land purchase, and Roshan Apna Ghar financing covers land purchase plus construction as a combined product, with up to 50% of the financing limit allocated for land.

Q17: Are there any taxes or charges on transferring money into my RDA from abroad? Remittances into RDA accounts are generally free of withholding tax and eligible for reward points under the Sohni Dharti Remittance Program (SDRP). Standard bank transfer charges may apply depending on your foreign bank.

Ready to Invest? Here’s Your Next Step

If you’ve been putting off buying property in Islamabad because the process felt unclear, complicated, or risky — the Roshan Digital Account system has removed most of those barriers. The legal framework is solid. The banking infrastructure is in place. And Islamabad’s property market, particularly in DHA, Park View City, and Gulberg Greens, continues to offer strong long-term value.

The key is getting the fundamentals right from the start: open your RDA first, fund it properly, verify your property thoroughly, and make every payment on record.

Bilal Estate and Builders specializes in helping overseas Pakistanis navigate Islamabad’s property market. Their team has hands-on experience with RDA-compliant transactions, from property shortlisting and legal verification to coordinating with bank nominees and registrar offices.

Whether you’re looking for a DHA plot, a ready house in Park View City, or a commercial investment in Islamabad — reach out to their team for a no-obligation consultation. You can also browse their current Islamabad listings to get a sense of what’s available in your budget.

Your money belongs in something real, legal, and yours. The Roshan Digital Account makes that possible — you just need to take the first step.

Trusted Sources and Further Reading

- State Bank of Pakistan – RDA FAQs — Official SBP guidance on Roshan Digital Account rules, property investment, and repatriation.

- ProPakistani – RDA Inflows Report (May 2026) — Latest statistics on RDA growth and diaspora investment.

- Bilal Estate and Builders – Islamabad Properties — Verified property listings in DHA, Bahria Town, Park View City, and CDA sectors.

Article last updated: May 2026. All financial figures are based on publicly available SBP and government data. This article is for informational purposes only and does not constitute legal or financial advice. Consult a qualified advisor before making property investment decisions.