pakistan budget 2026-27 real estate tax

Source: Finance Bill 2026 · FY2026-27 · Effective 1 July 2026 Published: June 2026 | bilalestateandbuilders.com

Quick Answer — Read This First

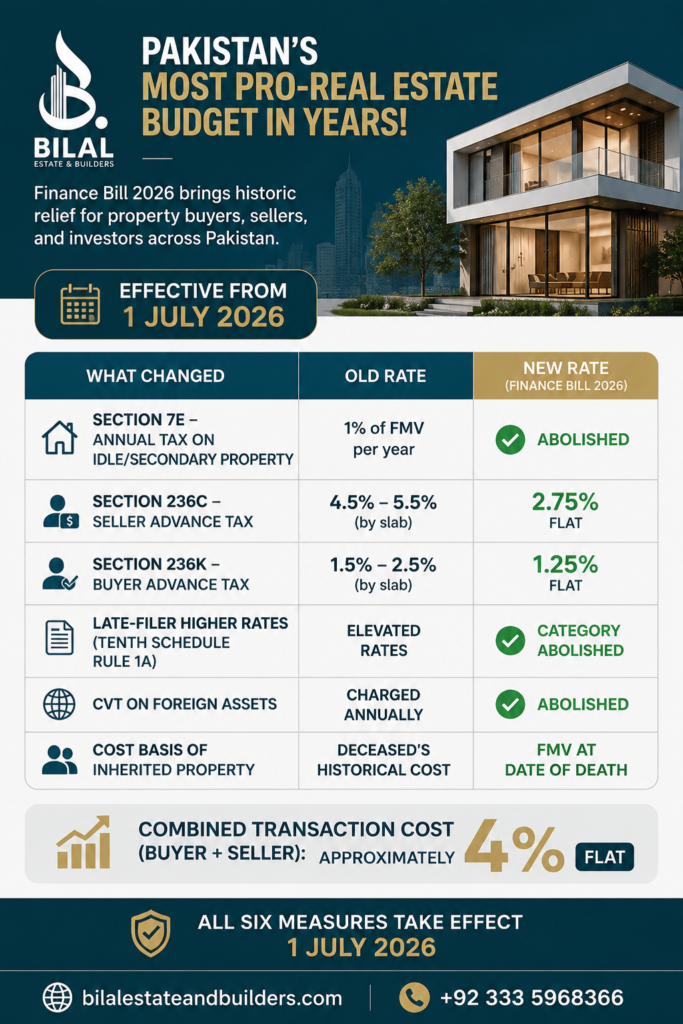

Pakistan’s Finance Bill 2026 is the most pro-real-estate budget in years. Here is what changed, effective 1 July 2026:

What Changed Old Rate New Rate (Finance Bill 2026) Section 7E — annual tax on idle/secondary property 1% of FMV per year Abolished Section 236C — seller advance tax 4.5%–5.5% (by slab) Flat 2.75% Section 236K — buyer advance tax 1.5%–2.5% (by slab) Flat 1.25% Late-Filer higher rates (Tenth Schedule Rule 1A) Elevated rates Category abolished CVT on foreign assets Charged annually Abolished Cost basis of inherited property Deceased’s historical cost FMV at date of death Combined transaction cost (buyer + seller): approximately 4% flat. All six measures take effect 1 July 2026.

The Problem That Kept Pakistan’s Property Market Frozen

Here is a scene that has played out hundreds of times across Rawalpindi, Islamabad, and Lahore over the past three years.

A buyer agrees on a plot price. Shakes hands. Feels good about the deal. Then he sits with the agent to calculate the full transfer cost — and the number is 12%, 15%, sometimes 18% of the transaction value.

Not one number. A pile of them.

Section 236K. Section 236C. Section 7E. Capital Gains Tax. Stamp duty. DC rates. Filer rate. Late-filer rate. Non-filer penalty. Slab one, slab two, slab three.

Nobody warned him. Nobody explained it clearly. And now a plot he thought cost PKR 1 crore is actually costing PKR 1.15 crore just to transfer — plus PKR 5 lakh every year if the property value exceeds PKR 2.5 crore.

This was Pakistan’s property tax reality from 2022 to June 2026. Complex. Punishing. Opaque.

The Finance Bill 2026 changes all of it — with effect from 1 July 2026.

This article uses the confirmed Finance Bill 2026 rates (not media estimates or proposals) to explain every change in plain language — what it was, what it is now, what it means for your wallet, and what you should do next.

The 6 Changes at a Glance

Before we go deep, here is the full picture in one place:

| # | Change | What It Means |

|---|---|---|

| 1 | Section 7E abolished | No more annual tax on your second property or idle plot |

| 2 | Section 236C → 2.75% flat | Seller pays less, and the same rate regardless of property value |

| 3 | Section 236K → 1.25% flat | Buyer pays less, and the same rate regardless of property value |

| 4 | Late-filer category removed | Only two categories now: filer and non-filer |

| 5 | CVT on foreign assets abolished | Overseas Pakistanis with declared foreign property get relief |

| 6 | Inherited property → FMV at date of death | Capital Gains Tax on inherited assets now calculated fairly |

Change 1 — Section 7E: The Annual Tax That Should Never Have Existed

What Was It?

Section 7E was introduced in 2022. It targeted anyone holding property worth more than PKR 25 million.

Here is exactly how it worked in three steps:

Step 1: FBR looked at your property’s assessed (FMV) value. Step 2: FBR declared that you “earned” 5% of that value as rental income — even if the property was empty and generating nothing. Step 3: A 20% tax was applied on that fictional income.

Net result: You paid 1% of your property’s FMV every single year — whether the property earned anything or not.

Real Example

You own a vacant plot in Rawalpindi. FBR fair market value: PKR 50 million

Section 7E calculation:

- Deemed income = 5% × 50M = PKR 2.5 million

- Tax at 20% = PKR 500,000 per year

Your plot earned: PKR 0 Your tax bill: PKR 5 lakh every year

Property owners, tax lawyers, and courts fought this for years. In May 2026, the Federal Constitutional Court declared Section 7E unconstitutional and void from the day it was introduced. The Finance Bill 2026 then formally abolished it.

What This Means For You

✅ No more annual tax on vacant plots or undeveloped land

✅ No more annual tax on your second, third, or fourth property

✅ Overseas Pakistanis holding property in Pakistan no longer carry this hidden yearly burden

✅ Investors with multiple high-value properties can now calculate true holding costs

Paid Section 7E in previous years? The court declared it void ab initio — meaning it was never legally valid from the start. Whether you can claim a refund for past payments is a legal question. Consult a registered tax practitioner to assess your specific situation.

Change 2 — Section 236C: Seller Tax Drops to a Flat 2.75%

What Is Section 236C?

This is the advance tax the seller pays when transferring property ownership. It is collected at the registry before the deal is completed.

Old vs Confirmed New Rate

Under the old system, your rate as a seller depended on the property’s value — the higher the value, the higher the percentage. This sliding slab made calculations confusing and penalised larger transactions.

| Seller | Old Rate | Finance Bill 2026 Rate |

|---|---|---|

| Active Filer | 4.5% / 5.0% / 5.5% (by value slab) | Flat 2.75% of gross consideration |

| Late Filer | Elevated rate (higher than filer) | Same as filer (late-filer category abolished) |

| Non-Filer | 10%+ | Remains high |

The rate is now calculated on gross consideration (the actual transaction price), not FBR notified value alone. Confirm with your lawyer or agent which value applies to your specific deal.

What This Saves You

| Property Value (PKR) | Old Seller Tax (5%) | New Seller Tax (2.75%) | Saving |

|---|---|---|---|

| 50 lakh | 2,50,000 | 1,37,500 | 1,12,500 |

| 1 crore | 5,00,000 | 2,75,000 | 2,25,000 |

| 3 crore | 16,50,000 | 8,25,000 | 8,25,000 |

| 5 crore | 27,50,000 | 13,75,000 | 13,75,000 |

Capital Gains Tax still applies separately. Section 236C is the advance withholding tax at registry. Your CGT on profit is calculated when you file your annual return. The two are separate.

Change 3 — Section 236K: Buyer Tax Drops to a Flat 1.25%

What Is Section 236K?

This is the advance tax the buyer pays at the time of property transfer. You pay this at the registry — before you receive possession.

Old vs Confirmed New Rate

| Buyer | Old Rate | Finance Bill 2026 Rate |

|---|---|---|

| Active Filer | 1.5%–2.5% (by value slab) | Flat 1.25% of fair market value |

| Late Filer | Elevated rate | Same as filer (late-filer category abolished) |

| Non-Filer | Very high (10.5%+) | Remains high |

Drafting note: The Finance Bill’s Salient Features memorandum states 1.5%, but the operative First Schedule text states 1.25%. The operative text governs unless corrected before enactment. Track the final gazette notification.

What This Saves You

| Property Value (PKR) | Old Buyer Tax (1.5%) | New Buyer Tax (1.25%) | Saving |

|---|---|---|---|

| 50 lakh | 75,000 | 62,500 | 12,500 |

| 1 crore | 1,50,000 | 1,25,000 | 25,000 |

| 3 crore | 4,50,000 | 3,75,000 | 75,000 |

| 5 crore | 7,50,000 | 6,25,000 | 1,25,000 |

Overseas Pakistani note: FBR already allows non-resident overseas Pakistanis (spending fewer than 183 days per year in Pakistan) to claim filer-equivalent rates under 236K — even if not on the ATL. With the rate now dropping to 1.25%, this benefit becomes even more valuable for the diaspora.

Change 4 — Late-Filer Category Abolished

This is a change many people have missed — and it is significant.

Under the old system, there were three categories for property tax purposes:

- ✅ Active Filer → lowest rates

- 🟡 Late Filer → elevated rates (punished for filing late)

- ❌ Non-Filer → highest rates

The Finance Bill 2026 eliminates the late-filer category entirely under Tenth Schedule Rule 1A.

Going forward, there are only two categories:

- ✅ Filer → 2.75% (seller) + 1.25% (buyer)

- ❌ Non-Filer → high rates (unchanged)

If you filed your tax return late in previous years and were classified as a late filer, you now qualify for full filer rates from July 1, 2026 — provided you are on the ATL.

Check your ATL status at fbr.gov.pk/verifyAtl — you need your CNIC. It takes 30 seconds and determines everything about your tax rates.

Change 5 — CVT on Foreign Assets Abolished

If you are a Pakistani resident who declared foreign property in your FBR tax return — a flat in Dubai, a house in the UK, an apartment in Canada — you were previously charged Capital Value Tax (CVT) annually on those foreign assets under FA 2022.

Finance Bill 2026 abolishes this completely.

This is especially relevant for:

- Overseas Pakistanis who maintain dual tax residency

- Pakistani residents with investments abroad who were penalised for honest disclosure

- Anyone considering consolidating remittances and investments back into Pakistan

Removing CVT on foreign assets removes a major disincentive to declare overseas wealth honestly — which is good for tax compliance and good for attracting foreign remittances into documented channels.

Change 6 — Inherited Property Now Valued at FMV at Date of Death

This is the most technical change — but for families inheriting property, it is transformative.

The Old Rule (and the Problem)

Under the old system, when you inherited a property and later sold it, Capital Gains Tax was calculated on the difference between the deceased’s original purchase price (historical cost) and your sale price.

The problem: If your father bought a plot in 1995 for PKR 2 lakh and you sell it in 2026 for PKR 80 lakh, your “gain” for tax purposes was PKR 78 lakh — even though you never paid PKR 2 lakh for it and the property appreciated over 30+ years during someone else’s ownership.

You were taxed on gains you did not personally make.

The New Rule

Under Finance Bill 2026, the cost basis of inherited property is stepped up to the Fair Market Value at the date of death of the deceased.

What this means in practice:

Your father passes away in 2024. At that time, the FMV of his Rawalpindi plot is PKR 70 lakh. You inherit the property. You sell it in 2027 for PKR 85 lakh.

Old CGT calculation: 85L − 2L (father’s 1995 purchase price) = PKR 83 lakh gain → taxed New CGT calculation: 85L − 70L (FMV at date of death) = PKR 15 lakh gain → taxed

You only pay CGT on the gain made during YOUR ownership period.

This is a fundamental fairness correction. Inherited property is not a windfall — it is a transfer. Taxing inherited gains at the historical cost of the deceased was always unjust.

Who Benefits

- Anyone who has inherited or is likely to inherit property

- Families settling estates where property values have appreciated significantly

- Children and legal heirs selling inherited property they did not personally develop or invest in

This change also has implications for estate planning and how families should document fair market valuations at the time of a relative’s passing. Keep formal FMV records — they become your CGT cost basis.

The Full Transaction Cost Under Finance Bill 2026

Here is what it now costs to buy and sell a property as an active filer, effective 1 July 2026.

Buying a Property — Active Filer (Example: PKR 1 Crore FMV)

| Cost | Rate | Amount |

|---|---|---|

| Section 236K (buyer advance tax) | 1.25% | PKR 12,500 |

| Stamp Duty (provincial) | ~1–1.5% | PKR 10,000–15,000 |

| CVT (provincial) | ~1% | PKR 10,000 |

| Registration Fee | ~0.5% | PKR 5,000 |

| Total Estimated | ~3.75–4.25% | ~PKR 37,500–42,500 |

Selling a Property — Active Filer (Example: PKR 1 Crore Gross Consideration)

| Cost | Rate | Amount |

|---|---|---|

| Section 236C (seller advance tax) | 2.75% | PKR 27,500 |

| Capital Gains Tax | Depends on purchase date & profit | Separate calculation |

| Total (excl. CGT) | 2.75% | PKR 27,500 |

Combined Round-Trip Cost (Buy + Sell, Filer, excl. CGT)

Approximately 4% flat — compared to 12–18% under the old system for many investors.

Filer vs Non-Filer: The Gap Is Still Real

Finance Bill 2026 rewards compliance heavily. If you are not on the ATL, the new rates do not apply to you.

| Active Filer | Non-Filer | |

|---|---|---|

| Buyer Tax (236K) | 1.25% | High (10.5%+) |

| Seller Tax (236C) | 2.75% | High (10%+) |

| Section 7E | Abolished (for everyone) | Abolished (for everyone) |

| CVT on Foreign Assets | Abolished (for everyone) | Abolished (for everyone) |

| Late-Filer Category | Abolished | — |

Single most important thing you can do today: Check your ATL status. Go to fbr.gov.pk/verifyAtl → enter your CNIC → confirm you are listed as active. If you are not listed, file your return before transacting. The difference in tax can be hundreds of thousands of rupees.

What Has NOT Changed — Be Honest With Yourself

Capital Gains Tax Remains

CGT is still in force. Properties purchased after July 1, 2024 are subject to a flat 15% CGT on profit — regardless of how long you hold them.

Properties purchased before July 2024 still benefit from the older reducing-slab CGT structure (lower rates with longer holding periods, potentially 0% after several years).

Section 236C (2.75%) and CGT are separate. You pay 236C at registry. You account for CGT in your annual tax return.

Non-Filers Still Pay High Rates

Finance Bill 2026 does not forgive non-compliance. If you are not on the ATL, your transaction costs remain punishingly high. There is no workaround.

Finance Bill Still Needs Final Assent

The budget was presented on 12 June 2026. These rates require National Assembly approval and presidential assent before they become law. The operative text governs over the summary documents — track the official Finance Act 2026 gazette notification before finalising large transactions.

There is also a drafting discrepancy in Section 236K: the Salient Features document says 1.5%, but the operative First Schedule says 1.25%. The operative text governs unless corrected. Watch for the final gazette.

A Real Scenario: What This Looks Like in Practice

Scenario: Khalid is an overseas Pakistani based in Saudi Arabia. He wants to buy a 1 kanal plot in Bahria Town, Rawalpindi. Gross consideration: PKR 2 crore.

| Old System (FY25-26) | Finance Bill 2026 (from July 1) | |

|---|---|---|

| Buyer tax (236K) | 1.5% = PKR 30,000 | 1.25% = PKR 25,000 |

| Stamp Duty + CVT + Reg | ~2.5% = PKR 50,000 | ~2.5% = PKR 50,000 |

| Section 7E (annual) | 1% of FMV = PKR ~20,000/yr | PKR 0 |

| Year 1 total cost | PKR 80,000 + 20,000 = PKR 1,00,000 | PKR 75,000 (one-time only) |

Over 5 years of holding, Khalid previously would have paid an additional PKR 1,00,000 in Section 7E. Under Finance Bill 2026: zero.

And if he sells after 5 years at PKR 3 crore:

| Old System | Finance Bill 2026 | |

|---|---|---|

| Seller tax (236C) | 5% = PKR 1,50,000 | 2.75% = PKR 82,500 |

| Saving on sale alone | — | PKR 67,500 |

Total saving across the investment lifecycle: over PKR 1.5 lakh — on a 2 crore property.

Practical Checklist: What To Do Before 1 July 2026

✅ If You Are Planning to Buy

- [ ] Check ATL status: fbr.gov.pk/verifyAtl (CNIC required — 30 seconds)

- [ ] Confirm both FBR notified value AND provincial DC rate for your property

- [ ] Calculate total cost: 236K (1.25%) + stamp duty + CVT + registration

- [ ] If overseas Pakistani, confirm non-residency status (under 183 days/year in Pakistan) to access filer rates

- [ ] If possible, time your transfer after 1 July 2026 to benefit from Finance Bill 2026 rates

- [ ] Ask your agent for a written cost breakdown before signing anything

✅ If You Are Planning to Sell

- [ ] Know your purchase date — pre-July 2024 properties have better CGT treatment

- [ ] Calculate 236C at 2.75% (Finance Bill 2026 rate) + your CGT liability separately

- [ ] Keep your tax returns filed and current — late-filer category is abolished, but non-filer status still costs you significantly

- [ ] Do not underdeclare transaction value — FBR enforcement is stricter than ever

✅ If You Have Inherited Property

- [ ] Document the Fair Market Value of the property at the date of the deceased’s passing — this becomes your CGT cost basis under Finance Bill 2026

- [ ] Get a formal FMV valuation or FBR record from the date of inheritance

- [ ] Consult a tax practitioner before selling inherited property to calculate CGT correctly under the new stepped-up basis rules

✅ If You Are an Overseas Pakistani Investor

- [ ] Section 7E abolition removes your biggest annual holding cost on high-value properties

- [ ] CVT on foreign assets gone — simplifies your tax position if you have declared foreign property in Pakistan returns

- [ ] Lower buyer tax (1.25%) and seller tax (2.75%) make Rawalpindi and Islamabad properties significantly more accessible

- [ ] Contact Bilal Estate and Builders for market-specific guidance on NRP investment opportunities

Frequently Asked Questions

What are the confirmed property tax rates in Pakistan from July 2026? Per Finance Bill 2026: Section 236K (buyer) = 1.25% flat. Section 236C (seller) = 2.75% flat. These replace the old tiered slabs. Combined transaction tax for a filer = approximately 4%.

Is Section 7E completely removed in Budget 2026-27? Yes. The Federal Constitutional Court declared it unconstitutional in May 2026 and the Finance Bill 2026 formally abolishes it. There is no longer any annual deemed income tax on property worth over PKR 25 million.

What is Section 7E in simple terms? It was a tax of approximately 1% of your property’s FBR value — charged every year even if your property sat empty and earned nothing. It has now been abolished entirely.

What is the difference between Section 236C and Section 236K? 236K = buyer pays this at time of purchase (1.25% from July 2026). 236C = seller pays this at time of sale (2.75% from July 2026). Both are collected at the registry. Both are advance withholding taxes — adjustable against your annual income tax return.

Is the late-filer category still in effect? No. Finance Bill 2026 abolishes the late-filer elevated rate category (Tenth Schedule Rule 1A). From July 2026, there are only two categories: active filer and non-filer.

What is the new rule for inherited property tax in Pakistan? The cost basis for Capital Gains Tax on inherited property is now the Fair Market Value at the date of the deceased’s death — not their original historical purchase price. This means you only pay CGT on gains made during your own ownership period.

Are overseas Pakistanis eligible for filer tax rates under Finance Bill 2026? Yes. FBR rules allow non-resident overseas Pakistanis (spending fewer than 183 days per year in Pakistan) to access filer-equivalent rates under 236C and 236K. The Finance Bill 2026 rates (1.25% and 2.75%) apply to them.

What is CVT on foreign assets and is it removed? Capital Value Tax on foreign assets was an annual charge on foreign property declared in Pakistani tax returns. Finance Bill 2026 abolishes it completely.

Does Capital Gains Tax still apply after Budget 2026-27? Yes. CGT is not removed. Properties purchased after July 1, 2024 face a flat 15% CGT on profit. Properties purchased before that date still benefit from the older reducing-slab CGT structure. Section 236C is separate from CGT.

How do I check my FBR filer status? Go to fbr.gov.pk/verifyAtl and enter your CNIC number. If you appear on the Active Taxpayer List, you qualify for filer rates. If not, file your income tax return before your next property transaction.

What is the total cost to transfer property in Pakistan from July 2026? For an active filer: approximately 3.75–4.25% to buy (including stamp duty, CVT, registration + 236K) and 2.75% to sell (236C only, excluding CGT). Combined round-trip: approximately 4% flat.

Will property prices increase after Finance Bill 2026? Lower transaction costs increase buyer confidence and market liquidity, which historically supports price appreciation. The Rawalpindi-Islamabad corridor, DHA, Bahria Town, and CDA sectors are expected to see increased documented transaction activity.

Is there a drafting discrepancy in the 236K rate? Yes. The Salient Features memorandum states 1.5%, but the operative First Schedule text states 1.25%. The operative text governs unless corrected before enactment. Track the final Finance Act gazette notification.

Can non-filers buy property in Pakistan after July 2026? Yes, but at significantly higher rates. The Finance Bill 2026 reliefs (1.25% buyer tax, 2.75% seller tax) apply to active filers only. Non-filers remain at elevated rates. For transactions above PKR 100 million, an Eligibility Certificate may also be required.

Should I complete my property transaction before or after July 1, 2026? If you are an active filer, waiting until after July 1, 2026 (and Finance Bill assent) means lower 236K and 236C rates. However, do not delay a strong deal purely for timing. Calculate both scenarios with your agent and make an informed decision.

Why This Budget Is Different — The IMF Connection

Pakistan is operating under an IMF Extended Fund Facility with an FBR revenue target of PKR 15.3 trillion for FY27. Cutting property taxes sounds counterproductive to hitting that target.

But the IMF agreed. Why?

Because the old system was generating less revenue, not more. High transaction taxes pushed deals underground. Properties were undervalued on paper. Informal power-of-attorney arrangements replaced formal registry. FBR collected nothing from grey-market deals.

The logic of Finance Bill 2026 is straightforward:

A 1.25% buyer tax on a fully documented, FBR-registered PKR 5 crore deal generates more real revenue than a 2.5% tax on a PKR 2 crore declared value on the same property — with the rest transacted off the books.

Lower rates + more documented transactions = higher total collections.

The construction sector, real estate developers, and the broader economy benefit too. When property moves formally, cement, steel, and labour move with it.

Ready to Invest? Talk to an Expert Who Knows These Markets

Knowing the rates is one thing. Knowing which areas, which projects, and which transaction structures work best for your situation is another.

Bilal Estate and Builders specialises in Rawalpindi and Islamabad real estate — with expertise in FBR valuation zones, DC rates across Bahria Town, DHA, Gulberg Greens, and CDA sectors, and the practical implications of Finance Bill 2026 for buyers, sellers, and overseas investors.

Whether you are buying your first home, expanding your portfolio, or investing from abroad get a clear cost picture before you commit

Sources

- Business Recorder — Real estate sector tax cuts, Budget 2026-27

- Profit by Pakistan Today — FCC declares Section 7E unconstitutional, May 2026

- Bloom Pakistan — IMF agrees to property tax cuts in Budget 2026-27

- FBR Active Taxpayer List — Verify Your Status

⚠️ Disclaimer: This article reflects confirmed provisions in the Finance Bill 2026 as presented on 12 June 2026. Rates become legally operative only after the Finance Bill receives presidential assent and FBR issues official gazette notifications. A drafting discrepancy exists in Section 236K (1.5% in Salient Features vs 1.25% in operative First Schedule text) — the operative text governs unless corrected before enactment. Always consult a qualified tax advisor or legal practitioner before completing any property transaction. Last updated: June 2026.